MONDAY, JANUARY 25, 2016

|

Trevor Tarpinian, CEPA®

Licensed Insurance Counselor

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

trevor@tfi4insurance.com

|

|

Disability Income Insurance 101 - Future Benefit

|

|

Most long term disability policies offer some type of future options to buy more coverage. This could be called the Benefit Update (BU), Additional Increase Option (AIO), Future Purchase Option (FPO), or some variation therein. This feature is strategic for a couple reasons. If you purchase your policy at a young age, odds are your income will grow with time. This coverage gives you the option to purchase more coverage down the road if your income warrants it. It is incredibly powerful, because most companies do not require medical underwriting again to exercise the

|

|

options. If you have a policy and now have health issues that would make applying for more coverage difficult or impossible, the increase option is going to essentially turn a blind eye. The only thing you need to prove is that your income justifies the coverage increase.

Let's look at several aspects to increasing your long term disability benefit with a future increase option.

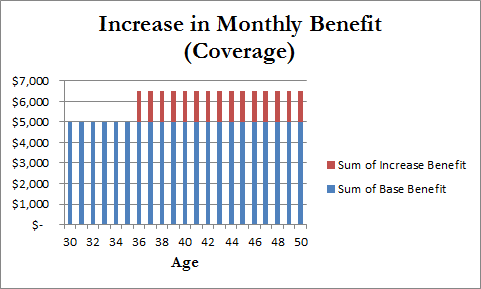

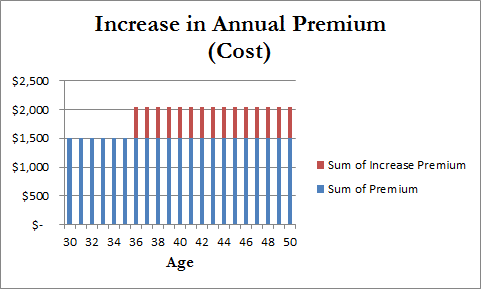

Pricing of Additional Coverage: When you exercise the option to buy more coverage, you are buying more coverage. It's not a freebie. Although your health rating will be locked in from the original policy, the pricing on the additional coverage will be based on your future age. See my illustration below if you were to buy $5,000 of benefit at age 30 and another $1,500 at age 36.

Age: There are usually age restrictions. Generally, you need to exercise any options by age 45, but these parameters are company specific.

Frequency: Companies vary with how frequent the window opens up to exercise the increase option. Typically, you'll get your option every 2-3 years, over the course of 7-10 years.

Increase Cap: This is perhaps the most important aspect to an increase option and one that throws many people a curve ball. Not all policies are created equal. Despite how great your income may have grown, some policies cap the amount of benefit increase by a flat rate ($3,000/monthly benefit; $4,000/monthly benefit; $5,000...etc.). They may cap it by a percentage of the base policy. If you originally signed up for $4,000 of monthly benefit, the increase option language may limit an increase to 50% of base policy - meaning the most you'll be able to increase is another $2,000 of monthly benefit.

Maximum Policy Benefit: Remember, your policy has a default maximum monthly benefit the policy and company will allow. It's probably somewhere between $10,000-15,000 of monthly benefit. If you already have $14,000 of monthly coverage and your earnings increase and you want more coverage, you're not getting more than a $1,000 monthly benefit increase from the increase option if your monthly benefit maximum limit is $15,000/month.

Exclusions: If you had any exclusions placed on the original policy (due to mental/nervous health history, back/spine issues, etc), you may not have an increase option benefit. Usually companies do not offer an increased benefit if an exclusion is on the policy. If you feel your exclusion is no longer appropriate, contact me about the possibility of removing it. Best case scenario is that we can get an exclusion removed and have the increase benefit added as a result.

Practical Application: I cannot stress enough that all companies and policies are different. Let me give you two examples:

1.) I had a client that started a very small disability income policy several years ago when he was young - just something to get things started and lock-in his health and insurability. After discussing career goals and income projection, I presented one particular company. It wasn't the cheapest thing on the planet, but I emphasized that we'd be able to increase coverage down to road up to $15,000 of monthly benefit with no limitations on the increase. If he made the money and could prove it, we could insure it. Fast-forward a few years and his income increased. He wanted more coverage. With no medical exam and just a few signatures we increased coverage from $1,600 to $15,000 of monthly benefit.

2) I had someone reach out to me this month asking about increasing their monthly benefit since their increase option window was open. (FYI - Not my client. I didn't write the original policy). The original policy had $4,000 of monthly benefit on it and when this person contacted me, they asked why they couldn't increase more than $2,000 of monthly benefit (for a total of $6,000), despite the fact that their increased income over the years justified even more coverage.

|

|

The answer was simple. Their particular policy and company has a percentage cap on the increase option - not to exceed 50% of the original coverage amount. Since the original policy coverage was $4,000, they wouldn't be able to increase the policy by more than $2,000. They've exhausted this policy and if they want more than $6,000 of monthly benefit, they'll have to buy a second policy, do another physical, and be medically insurable. Their policy and company is a major name in the disability insurance world, particularly with medical professionals. If the cost of the initial policy was comparable in both scenarios, which one would you prefer? You want options, but what kind of options are you getting? Are they limited? You also buy your financial representative with your policy. Are you getting the experience you deserve to maneuver through the options you need?

Click the "Contact Us" button and reach out to me with questions on increasing the coverage on your policy.

|

|

No Comments

Post a Comment |

|

Required

|

|

Required (Not Displayed)

|

|

Required

|

All comments are moderated and stripped of HTML.

|

|

|

|

|

|

NOTICE: This blog and website are made available by the publisher for educational and informational purposes only.

It is not be used as a substitute for competent insurance, legal, or tax advice from a licensed professional

in your state. By using this blog site you understand that there is no broker client relationship between

you and the blog and website publisher.

|

Blog Archive

2022

2021

2018

2017

2016

2015

|